Authored by Jared Walczak of the Tax Foundation in association with Alaska Policy Forum.

A copy of the PDF version can be found here.

Click here for a PDF copy of the policy brief.

Key Findings

- Alaska’s heavy reliance on oil and gas taxes and investment income creates extreme revenue volatility and complicates revenue forecasts.

- Alternative revenue streams cannot easily displace existing sources. For example, to raise as much of its revenue from an income tax as the average state does, Alaska would need to have income tax burdens three times as high as California’s.

- Alaskans experience a higher-than-average cost of living, partially offset by higher wages, but this yields an additional federal income tax liability greater than the amount residents of many other states pay in state income taxes.

- The economic literature demonstrates that income taxes promote outmigration and reduce in-state employment mobility, gross state product, investment, and innovation.

- Individual income taxes have a twofold effect on small businesses: directly as a tax on owners’ income and indirectly by driving up labor costs.

- Most states are reducing reliance on individual income taxes; 21 states have enacted or implemented individual income tax rate cuts since 2021 while only New York and the District of Columbia have raised rates.

- A state sales tax would be more economically neutral, and the ability to design one from scratch would allow lawmakers to avoid some of the design features that make the sales tax regressive.

- No new state tax will be sufficient on its own; additional fiscal restraint will be necessary, perhaps in the form of an enhanced spending cap.

Introduction

The global pandemic put many plans on the backburner—some because they ceased to be important in relative terms, and others because they ceased to matter in absolute terms. For many states, the pandemic era has been one of unexpectedly strong tax revenues, thus sidelining most talk of new or higher taxes. For Alaska, with its relative geographic isolation and heavy reliance on the energy industry, fiscal relief came later. But it arrived nonetheless, on the wings of higher oil prices.

When oil prices were in relentless decline, Alaska lawmakers were broaching difficult questions about whether the state required a new revenue source, like an income or sales tax. But then the state’s large reserve funds began yielding impressive investment returns and oil revenue started flowing again. The timeline was pushed back on any fiscal reckoning.

Lawmakers know, however, that there are still threats to the state’s revenue sources, and that their deliberations have been postponed, not canceled. This publication is about Alaska’s options when the reprieve is over and ordinary revenue trends reassert themselves.

Policymakers will once again debate implementing either an income tax or sales tax, restraining spending, or pursuing some combination of these options. Their deliberations should be guided by economic research and other states’ experiences, considering the trade-offs associated with the proposed new taxes.

Both an income and a sales tax would create economic drag, but an individual income tax would have a much larger negative impact on the state’s competitiveness, growth, and economic diversification. The pages that follow document the challenges lawmakers face, review the economic literature on available tax options, and tackle questions about thorny issues surrounding the implementation of a new tax or novel ideas like seasonal taxation.

Alaska is one of nine states without a wage income tax and one of five states without a state-level sales tax. Alaska and New Hampshire are the only states with neither. Perhaps this distinction will be maintained, or perhaps not—but an income tax in particular has the potential to undermine much of what lawmakers wish to accomplish.

Budgeting in a Unique Economic Environment

They don’t call Alaska “America’s Last Frontier” for nothing. The state, with its geographic isolation, climate, abundant natural resources, and unique employment patterns—to cite only a few of the many ways Alaska adds diversity to the U.S.—does not readily answer to national economic generalizations. The cost of living is higher. The cost of providing government services to a broadly dispersed, low density population is markedly higher. The industry mix is different. Residency patterns diverge from national norms. It is little wonder that the state charts its own course in many ways, including in state taxation.

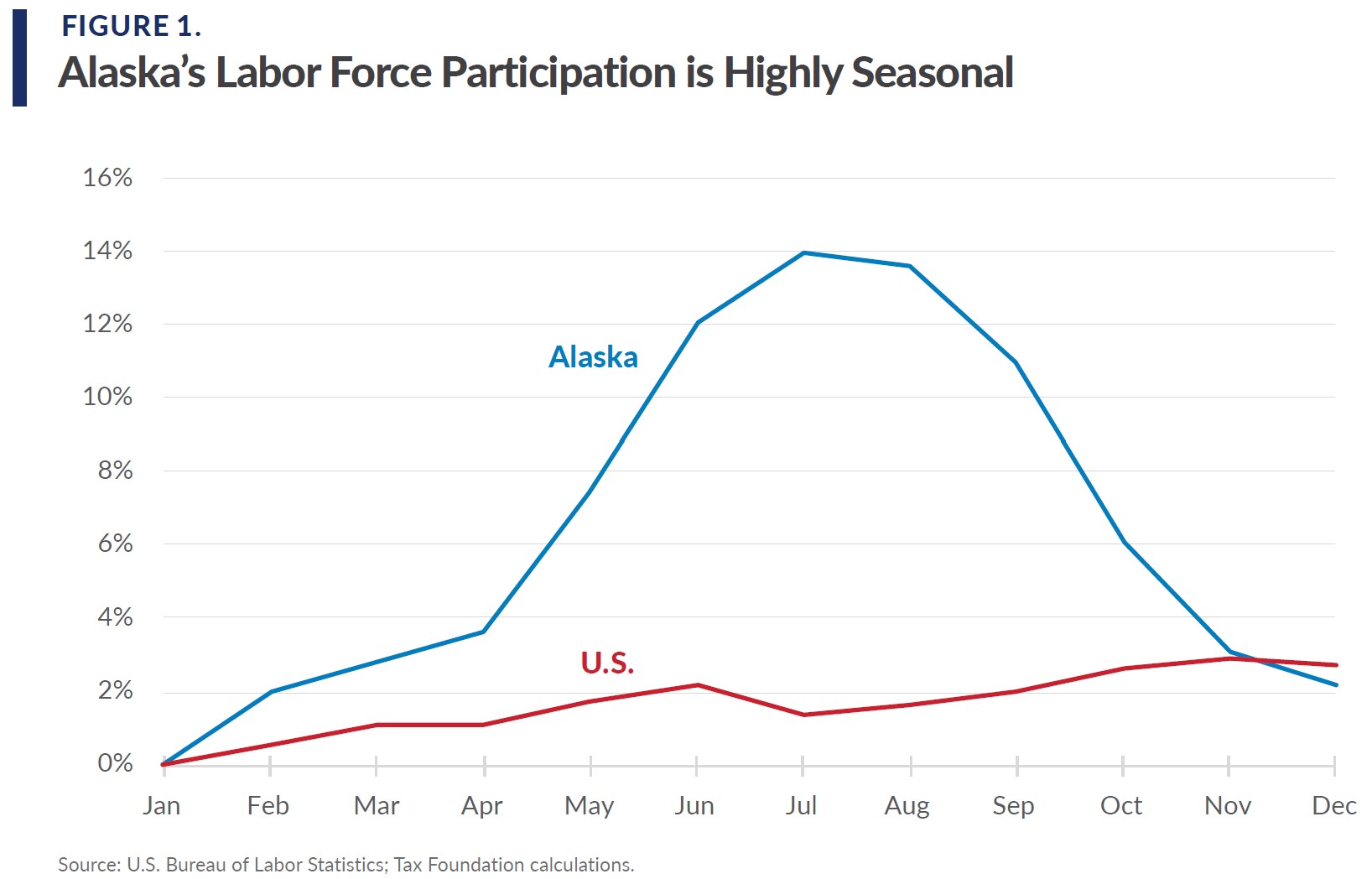

Alaska is a state of abundant resources, combined with remoteness and a challenging topography. And many of the state’s salient features—its oil and gas deposits, fisheries, and tourist draw—lend themselves to highly seasonal employment.

For both Alaska and the nation as a whole, January tends to be the low point in labor force participation, after temporary employment to keep up with the holiday rush has lapsed. Nationally, while summer employment is only about 2 percent higher than January employment and peak employment comes at the end of the year, Alaska’s employment patterns are highly seasonal, with July’s labor force 14 percent larger than January’s, on average, over the past two decades.1

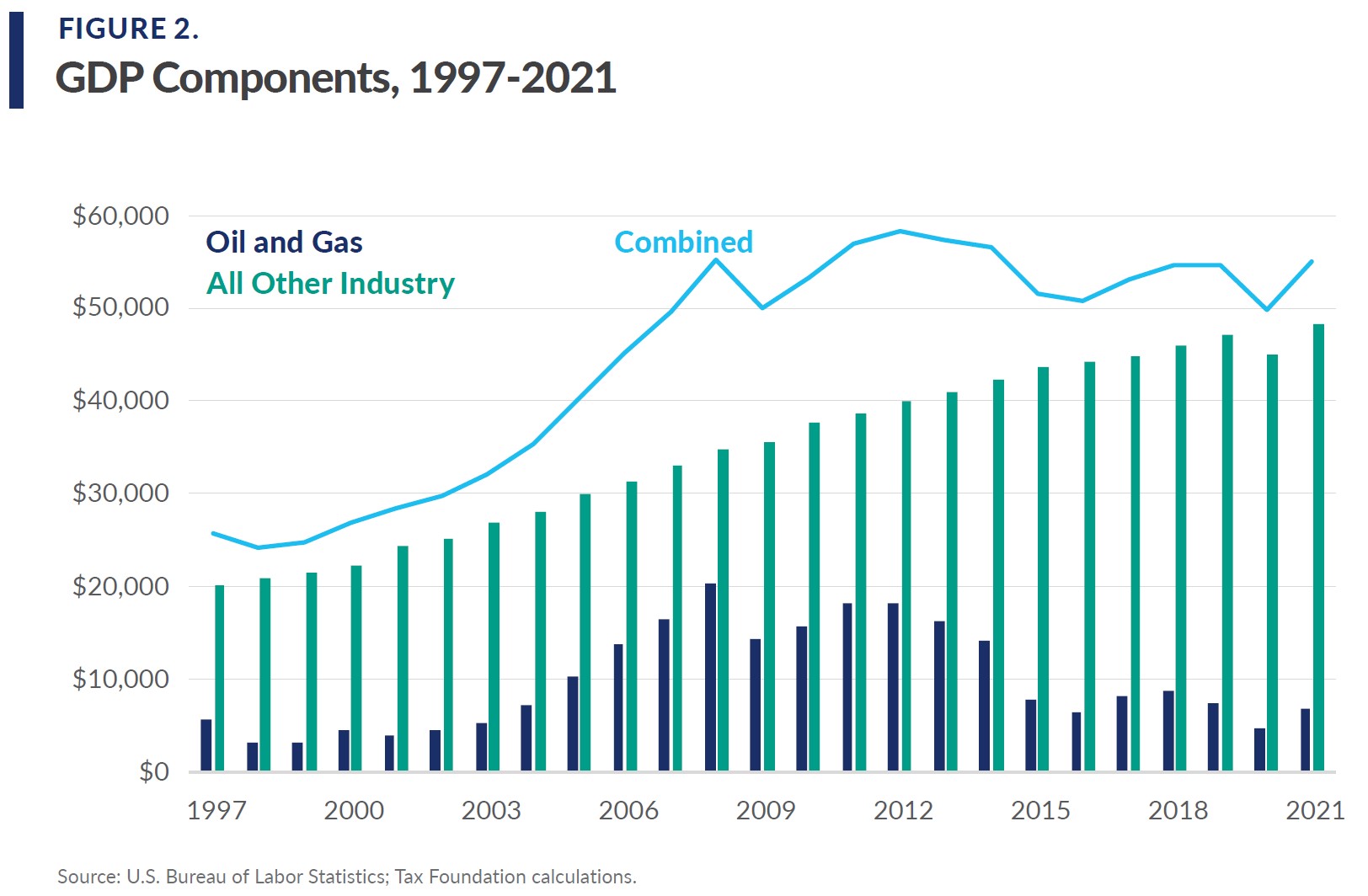

All employment exists in symbiosis to some extent; businesses enjoy innate complementarity. But Alaska’s economy is heavily dependent on a few key industries, with most of its other activity falling into a range of supportive services. Not even one in 200 Alaskan wage earners is directly employed in the oil and gas industry, yet the industry is responsible for about 22 percent of gross state product in any given year, peaking at 37 percent in 2008 and most recently settling at 12 percent in 2021.

Twelve percent is quite substantial, but not overwhelming. Nevertheless, petroleum is expected to account for an estimated 81 percent of the state’s own-source non-investment revenue in FY 2023, and about 46 percent of all own-source income (since investment income, chiefly from past oil revenues, is expected to nearly match new petroleum revenues). The industry’s taxes contribute well above its relative share of the state’s economy, as sizeable as its share is.

Alaska’s oil industry employs relatively few people but makes a substantial contribution to gross state product. The state’s growth has largely been in support industries—those outside of basic industries like oil, fishing, and government, and which support Alaska’s largest industries—but this growth is not rapid enough to be transformative, and there are currently few, if any, candidates to join Alaska’s short list of basic industries. This lack of economic diversity exposes the state’s economy—and state revenues—to extraordinary volatility. If one or more of the basic industries took a long-term hit, the state’s funding streams would be seriously compromised.

Alaska’s heavy reliance on the energy sector is both a blessing and a curse, but it is undeniably the bane of revenue forecasters and lawmakers attempting to adopt budgets that rely on some degree of revenue stability. The most recent forecast for FY 2023 unrestricted general fund revenue is a healthy $8.3 billion, buoyed by high oil prices. Because the state releases 10-year revenue forecasts twice each year, this is only the latest in a long string of forecasts for FY 2023, and by far the most optimistic. Looking exclusively at spring forecasts, expectations for the current fiscal year’s revenues have ranged from a low of $1.7 billion (2016 forecast) to the current high of $8.3 billion.2

Figure 3 shows forecasts for the next decade, drawn from 10-year forecasts from the past decade. Distinct waves of outlooks are evident here, and lawmakers bracing for what they expected as of the late 2010s can breathe a sigh of relief right now.

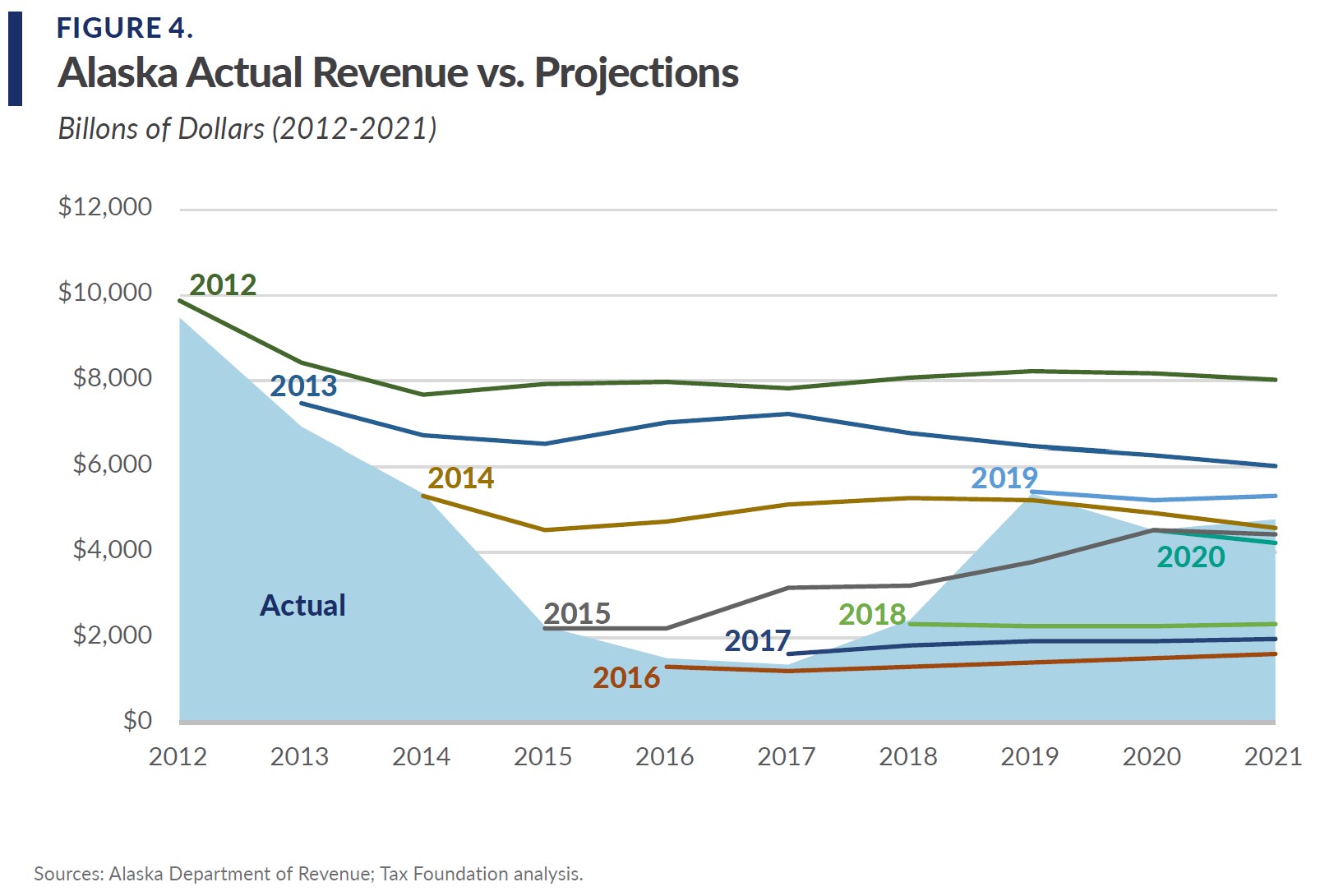

Though the most pessimistic forecasts did not come to fruition, the above chart is not a case for the triumph of optimism either. Forecasters completely missed the bottoming out of the oil market in the mid-2010s. A spring 2011 forecast anticipated that Alaska would generate $8.3 billion in general fund revenue in 2017; the actual figure was one-sixth the expectation, at less than $1.4 billion. Figure 4 shows actual revenues compared to projections for FYs 2012 through 2021. Almost invariably, forecasters assumed a general continuation of whatever trends existed at the time they issued their estimates. Admittedly, it is very difficult (perhaps almost impossible) to anticipate a decade’s worth of oil price fluctuations. But under Alaska’s current revenue structure, that is the task before the state’s economists and the challenge of lawmakers who must budget under this uncertainty and extreme fluctuation.

Lawmakers have responded to this revenue volatility by tapping the state’s extensive reserves, but those reserves are not limitless. They can smooth even extreme fluctuations in annual revenue if expenditures hew toward the long-run average of the state’s revenues and the fluctuations continue to revolve around a given mean. In practice, however, officials increasingly fear that energy markets will experience a secular (i.e., long-term) decline, even if they still enjoy boom years like the current ones within that broader trend.

Alaska and the “Problem” of Big Numbers

Alaska’s state revenues largely derive from taxes on the petroleum industry and from investment returns on the state’s substantial—but dwindling—reserve funds. The state’s long experience of extreme revenue volatility, combined with legitimate concerns about a long-term secular decline in oil prices, has many policymakers exploring ways to diversify Alaska’s revenue sources.

The sheer magnitude of the revenue Alaska has traditionally—if not always reliably—reaped from oil and gas production (and investment returns on past activity) makes a fiscal rebalancing with any alternative source of tax revenue exceedingly difficult. Alaska state revenues approached $30 billion in FY 2021—about $117,000 per household. This is not a typographical error. The median household income in Alaska is $77,640, and total personal income in the state was $49.2 billion in FY 2021. While some Alaskan incomes well exceed the median, Alaska’s state government revenues that year were 60.6 percent of state total personal income.

Of course, FY 2021 was an anomalously good year, the sort of year that would make discussions of additional sources of tax revenue moot. The state is only projecting $16.4 billion in FY 2023, a swing of $14 billion.3 But even then, state revenues should be about 34 percent of state personal income, compared to a national average of less than 13 percent. Buoyed by oil and gas revenue and investment returns on deposits from prior receipts, Alaska has by far the highest revenues per capita of all states, and traditional revenue tools might modestly supplement, but cannot come close to replacing any substantial loss of, Alaska’s unique revenue sources.

Alaska has had an income tax before. In fact, to date it is the only state to have repealed an individual income tax, doing so when the state’s oil fields started generating enough tax revenue to obviate the need for one. In 1980, the last year Alaska’s income tax was in operation, it generated $100.5 million, with a top rate of a now-astonishing 14.5 percent. Adjusting collections for inflation, an income tax with similar parameters would only have increased state revenue by 1 percent in FY 2021—a surprisingly modest effect for a tax with a top rate that would be the country’s highest.

To put this in perspective, states with wage income taxes generate, on average, about 13.1 percent of total revenue (and 43.3 percent of state tax collections) from the income tax. An Alaska income tax would have to raise $4.5 billion a year—over $17,600 per household—to have contributed that proportion to state collections in FY 2021, or about $2.5 billion in FY 2023 when the state projects total revenues of $16.4 billion. How high is $17,600 per household? In high-tax California, with a top marginal rate of 13.3 percent on the highest earners, and where even an individual making a little over $61,000 faces a 9.3 percent marginal rate, the income tax brings in less than $6,450 per household.

Alaska’s individual income taxes peaked as a percentage of tax revenue in 1975, when it was responsible for 47 percent of state tax collections, though a much smaller share of total revenues. Actual collections peaked in 1977 when they accounted for nearly 19 percent of all state revenues. For the final 15 years of the tax’s 22-year existence,4 its average contribution to state revenues was about 9.5 percent, though it fluctuated wildly from 2.8 to 18.8 percent. More precisely, it was the denominator—total revenue—that fluctuated so wildly. The state income tax, even when imposed at very high rates, did not generate nearly enough revenue to smooth over the volatility.

In FY 2023, only 8 percent of state revenue will come from non-petroleum and non-investment sources. This is substantially more than in the economic boom year of FY 2021, when all nonpetroleum and non-investment sources accounted for less than 3.5 percent of revenue. The volatility is all too real, but the sheer magnitude of these figures also demonstrates how difficult it will be to offset any significant volatility, let alone long-term decline, in revenues from existing sources. This is not an argument against acting: policymakers are right to be concerned about the long-term viability of the current revenue mix. It is, however, an argument for prudence, and particularly for ensuring that the economic costs of a new tax are not disproportionate to the modest contribution the new revenue makes to smoothing out state receipts.

Expenditure Constraints

Alaska’s constitution contains an appropriation limit, but its current parameters render it entirely ineffectual. The state spending cap has existed for over four decades, yet Alaska still spends much more than other states do, whether spending is measured per capita, as a percentage of income, or as a percentage of gross state product.

No one doubts that it is more costly to provide government services to sparsely populated regions and that everything from roads to schools to health services will cost more in Alaska. But when in 2020 the state spent 149 percent of the national average as a percentage of gross state product, 151 percent as a percentage of personal income, and 161 percent of the per capita average, it is not difficult to conclude that some constraints on future expenditure growth are warranted.

That Alaska has an expenditure limit,5 intended to curtail the growth of government, is not unusual; most states do. They vary, however, in their effectiveness, and Alaska’s appropriation limit is particularly toothless. It has many exclusions—some necessary, others arguably not—and allows an increase of appropriations of 5 percent per year in addition to inflation and population change adjustments. With capital projects excluded from the spending cap, and a very generous growth factor, it does little to constrain spending. And as a provision of general law, it can be overridden within the budget. Meanwhile, the constitution caps non-capital project, non-Permanent Fund appropriations at an inflation- and population-adjusted amount that currently stands at approximately $12 billion, also sufficiently high to accomplish little.6

It is difficult to see how additional taxes alone can backfill the revenue Alaska stands to lose if there is a long-term decline in oil prices or a reduction in demand. Meaningfully constraining future growth of government will have to be part of the bargain. This will require spending discipline and transforming the state’s constitutional spending cap and statutory appropriations limit from dead letters to actual policy constraints.

Alaska’s Existing Income Tax Premium

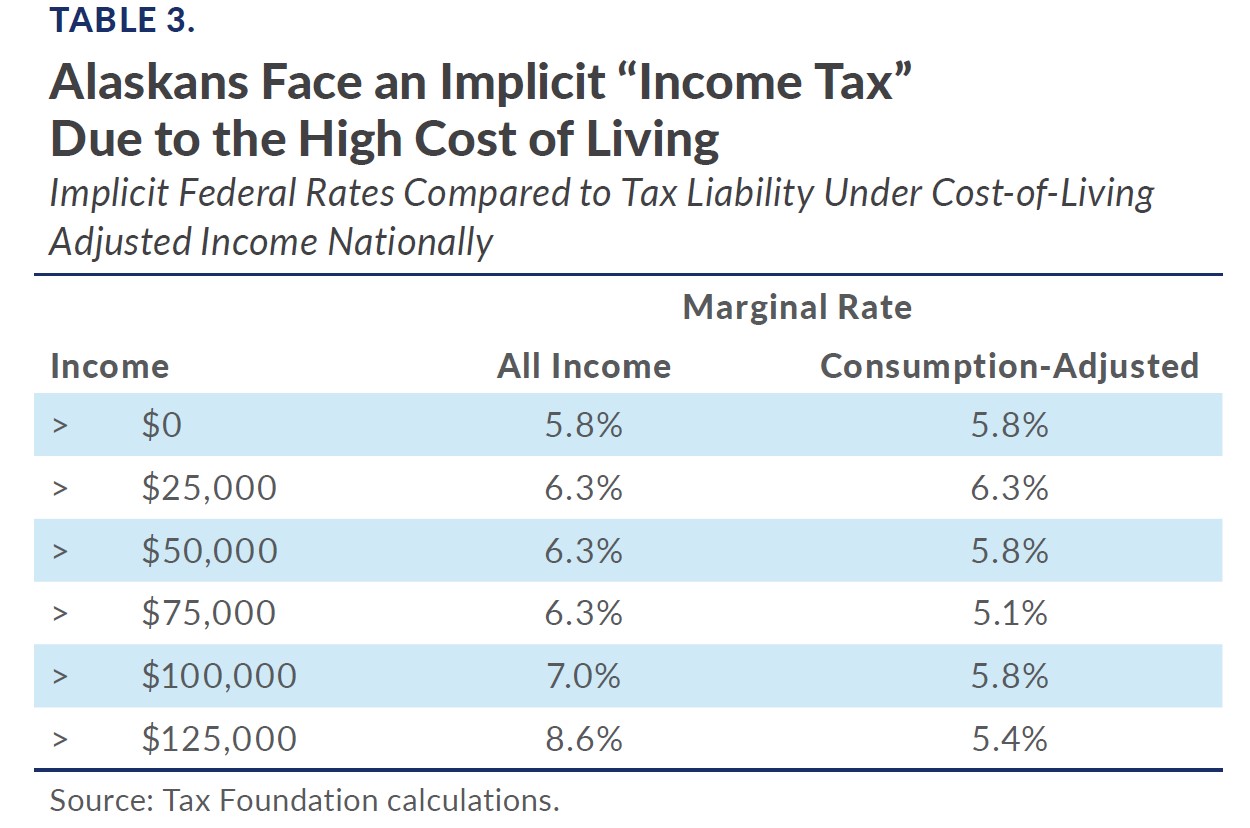

Living in Alaska is not cheap. Nationally, the median household income is just under $65,000. An Alaska household needs to earn almost $20,000 more than that—$84,427—just to break even on purchasing power, given the state’s high cost of living. Salaries tend to reflect this disparity, but the median household income ($77,790) is the equivalent of only $59,885 nationally and comes with an additional $4,888 in federal income and payroll tax liability for a married couple ($6,679 for a single filer).7

A higher cost of living is not a tax, but it does carry tax implications because more federally taxable income is necessary to purchase the same lifestyle that lower wages could purchase elsewhere. The following table shows the additional federal income and payroll taxes imposed on Alaskans compared to the taxes imposed on incomes with the same purchasing power parity nationally. For instance, $50,000 in Alaska purchases as much as $38,491 nationally, and taxpayers face an additional $3,964 (single filers) in income and payroll taxes on that $11,509 difference.

Of course, not all income is consumed—at least not immediately. At lower levels of income, very little is saved and functionally all income goes to present consumption, but higher earners have higher levels of savings and investment. While consumer costs are higher in Alaska, state residents have access to the same international investment market as taxpayers anywhere else in the country, so we ran the numbers a second time to yield a “consumption-adjusted” tax differential, taking into account the cost premium only on the estimated share of income devoted to personal consumption.

Notably, this federal tax differential results in a tax wedge similar to a high-rate income tax at the state level, mapping to a traditional graduated-rate schedule if the cost-of-living adjustment is applied to all income, and with somewhat more erratic “marginal rates” if the adjustment is only applied to the share of income consumed. Even with the more conservative approach, however, most married filers face the equivalent of an additional 5 to 6 percent on federal income and payroll taxes on the income necessary to secure the same purchasing power as their non-Alaskan peers.

The median top marginal income tax rate in the states is about 5 percent, and effective rates are, of course, lower, meaning that the additional federal income tax burden in Alaska will frequently exceed the burden of a state income tax elsewhere. In other words, when incomes are adjusted for purchasing power, Alaskans pay more in income taxes than most residents of states that impose their own income tax in addition to the federal one.

This premium does nothing for the state of Alaska’s bottom line. The mere fact of its existence does not solve any of the problems that proposals to impose a state income tax are intended to solve. These added costs are, however, highly salient to state taxpayers. They reduce fiscal capacity and make any additional tax—but especially a further tax on income—harder to bear.

The state and local tax (SALT) deduction can alleviate this burden somewhat, but only on the margin. Should Alaska impose an individual income tax, residents could deduct their state income and local property tax burdens—up to $10,000 per household under the current cap—from federal taxable income, which defrays the cost somewhat, but still leaves Alaskans far worse off than they would be in other states where the cost of living is lower.

The SALT deduction, moreover, is for the taxpayer’s choice of property taxes plus income or sales taxes, but not both. Currently, Alaskans deduct their municipal sales taxes (typically identified through a calculator and not based on actual documentation of purchases) plus any local property taxes. If atop the current system of municipal sales taxes the state implemented an income tax, most taxpayers would claim income and property taxes instead, losing the deduction for local sales taxes. Conversely, if Alaska adopted a state-wide sales tax, it would be deductible in addition to municipal sales tax burdens, up to the $10,000 cap.

Income Tax Trends

When Alaska policymakers repealed the state’s income tax more than four decades ago, they did not become trendsetters. The state’s capacity to do away with its largest tax was unique to place and circumstances, and to this day Alaska is the only state to have adopted and then repealed a tax on wage income. Two states, however, have recently enacted legislation repealing narrow taxes on interest and dividend income. And, more significantly, most states are now cutting their income taxes.8

The median top marginal rate of state income taxes was a full 2 percentage points higher in 1980(when Alaska’s tax was repealed) than it is today.9 Of the 44 states with any sort of income tax during the period, 31 states and the District of Columbia have lower top marginal income tax rates now than they did in 1980, while only nine have higher rates. The latter category includes Connecticut, which adopted its income tax in 1991, and Washington, which recently adopted a tax on the capital gains income of high earners.

If anything, the trend toward income tax reductions has accelerated in recent years. Since January 2021, 21 states have enacted or implemented individual income tax rate cuts, while only New York and the District of Columbia have raised rates.10

States’ recent rate cuts are a natural and appropriate response to both sustained state revenue growth and the enhanced mobility of individuals and businesses as remote and flexible work arrangements became more viable after the pandemic forced an experiment with remote work. Employees have more flexibility in choosing where to live, while employers can choose to locate somewhere with fewer concerns about access to a qualified white-collar workforce, since at least some of those hires can be made anywhere in the country.

Realizing the new state of competition, states are cutting taxes, and individual income taxes in particular, recognizing them as a driver of location decision-making and a damper on investment and entrepreneurial activity. But this is merely an acceleration of a longer-term trend of reducing income tax rates. When Alaska last imposed an income tax, it was one of 15 states (and the District of Columbia) with a top rate in the double digits. Today, only four states and the District of Columbia have a top rate that high. In 1979, only 10 states had top rates of 5 percent or lower. Today, 16 do.

Moreover, in the past year and a half, five states have adopted legislation transitioning their graduated-rate income taxes to single-rate taxes, with two more states potentially waiting in the wings. This would bring the number of states with flat taxes to 16.11 Only five states had flat taxes when Alaska last imposed an income tax and for the first time since Alaska’s decision to jettison its income tax, full repeal of several states’ income taxes is now within the realm of possibility. Currently, nine states forgo taxes on wage income. It is increasingly plausible the list could grow.

If Alaska considers an income tax now, it comes against the backdrop of states actively seeking to reduce their individual income tax burdens and using low (or no) income taxes as a meaningful competitive advantage.

Lessons From Other States

Only two states have adopted a wage income tax in the past half-century: Connecticut and New Jersey. The New Jersey tax was adopted in 1976, a few years before Alaska’s repeal, while Connecticut did not implement an individual income tax until 1991. In both states, the initial rates were relatively modest and the tax was sold as a way to reduce other existing tax burdens. And in both states, today’s rates are high—extremely high in New Jersey’s case—while taxpayers have not experienced any relief on other taxes.

New Jersey lawmakers long resisted an income tax. A front-page headline in The New York Times in May of 1975 read “Final Attempt to Enact Jersey Income Tax Fails”—and “final” certainly seemed like the right word. In a legislature with overwhelming Democratic majorities and a budget crisis precipitated in part by a new court mandate on a different set of revenue streams for education funding, Senate Democrats rejected income tax proposals four times in 10 months. It was the demise of the fourth proposal (for a 2.5 percent flat tax) that led Senate President Frank Dodd to declare that “a state income tax is dead.”12

A year later, after the state supreme court took the extraordinary step of closing all public schools until the legislature approved a different funding stream for them (the court objected to the state’s heavy reliance on local property taxes), the income tax idea was no longer dead. A divided legislature narrowly approved a two-bracket graduated rate tax with a top rate of 2.5 percent. Even lawmakers who voted for the tax disliked it and seemingly had no aspirations for it to do anything more than reduce reliance on local property taxes for school finance, in keeping with the court’s order. It was not intended to fund other state governmental programs.

Today, New Jersey’s top marginal income tax rate is 10.75 percent. And while judicial decisions did diversify education funding streams, this did not translate into lower property tax burdens. New Jersey’s top income tax rate is tied with the District of Columbia’s for the third highest in the country. But no tiebreaker is needed on property taxes, where New Jersey’s property taxes are far and away the nation’s highest, with an effective rate of 2.21 percent on owner-occupied housing, more than double the national average of 1.08 percent.13

Connecticut’s property taxes are also anomalously high, ranking fifth highest at 1.76 percent of housing value. And the sales tax, at 6.35 percent, is hardly low. When Connecticut lawmakers grudgingly adopted an income tax in 1991, they did so to allow a reduction in other taxes. Today, what began as a flat 4.5 percent income tax is now a seven-bracket tax with a top rate of 6.99 percent. Over the tax’s first three decades (1991-2021), revenue increased 136 percent on an inflation-adjusted basis.14

Like Alaska lawmakers, Connecticut policy leaders were wary of an income tax, with then-Gov. Lowell Weicker (I) saying he would only propose an income tax as “a last resort.” But the state increased its budget dramatically during an economic surge, leaving it unprepared for a revenue contraction during a recession. General fund expenditures soared 62 percent on an inflation-adjusted basis between FY 1983 and FY 1991, so when the revenue boom came to an end, lawmakers were left holding the bag. Despite fears that “imposing an income tax would be like pouring gasoline on a fire” during a recession, Weicker felt that he had little choice. Weicker’s successor, who initially pledged to repeal the tax, instead turned it into a graduated rate tax—initially a tax reduction, since the top rate remained at 4.5 percent. But once the principle was admitted, more changes followed, and by 2015, the top rate hit 6.99 percent.

The general trend in recent years has been to reduce income taxes, not increase them. But the last two states that initially adopted relatively low-rate income taxes, and then only under protest, soon discovered that their modest income taxes were subject to significant upward pressure and that narrow initial purposes soon gave way to more expansionist visions of government. It is a cautionary tale for Alaska and any other state considering the adoption of a new income tax.

The No PIT Advantage

Nine states forgo broad-based income taxes. (One, New Hampshire, currently taxes interest and dividend income but is phasing out the tax, while another, Washington, recently adopted a limited income tax on capital gains above $250,000.) Alaska’s income tax-free system has largely relied on revenues from oil and gas, an option not available to all states, but others—like Florida, New Hampshire, Tennessee, and Texas—have adopted different strategies to avoid taxing individual income.

Over the past decade, states that forgo income taxes have seen their populations grow at twice the national rate.15 And the ongoing migration from high- to low-tax states, and particularly states with low-income taxes, is likely to accelerate with the growing viability of telework post-pandemic. Increasingly, many people will be able to live wherever they wish. Those who are highly sensitive to taxes will find it easier than ever to relocate to jurisdictions with lower tax burdens, regardless of where their employer is located. And employers themselves will have more location flexibility as geography becomes less of a constraint on their workforces.

In Alaska, this may mean that back-office employees of Alaska-based companies are no longer bound to Alaska and could leave if their overall cost of living—which would take both taxes and the Permanent Fund Dividend into account—was lower elsewhere. It could also mean, more encouragingly, that people drawn to Alaska’s natural beauty could move to the state, either full-time or for part of the year, despite working for an employer located elsewhere.

The PIT as a Tax on Small Business

Alaska imposes a corporate income tax, which yielded 17,717 returns in FY 2020.16 The federal government, with its corporate income tax, only yielded 2,712 returns from Alaska. What accounts for the difference? Tax apportionment.

The federal government does not care about the states to which a company’s taxable income is sourced, so the 2,712 corporate income tax returns it associates with Alaska are the C corporations domiciled in Alaska. But Alaska itself—like all other states with corporate income taxes—is concerned not only with C corporations based in Alaska but also with out-of-state firms doing business in Alaska. Many corporations that are not domiciled in Alaska nonetheless have tax nexus in the state and generate income from sales sourced to the state, forming the basis of these tax obligations.

While corporate income taxes are apportioned, individual income taxes are not. Because they are imposed on individuals, not entities, they source income to either where it is earned or to the taxpayer’s residence. Most small businesses are pass-through businesses, whose owners pay individual income tax on their share of the business’s income rather than being subject to corporate income tax, meaning that not only would an individual income tax be—among other things—a tax on small businesses, but unlike the corporate tax, its primary business incidence would be on businesses whose owners live or work in Alaska.

In FY 2019 (most recent data), nearly 78,000 Alaskans reported pass-through business income on their federal income tax returns, a figure representing more than one-in-five federal filers from Alaska.17 Small businesses are over 99 percent of Alaska businesses and employ 52.4 percent of Alaskans.18 The overwhelming majority of these businesses are pass-through businesses that would be hit by an individual income tax. Ownership interests outside the state could not be taxed, except for income those owners earned while physically present in the state.

Corporate income taxes fall on capital investment to a far greater (and more detrimental) extent than individual income taxes do, but a state’s corporate tax—at least provided it is apportioned based on sales (as Alaska’s is)—does not uniquely burden in-state capital investment. The allocation of individual income taxes on pass-through businesses, however, tends to localize those costs of doing business in the state, and the tax would fall on many of the businesses and industries that Alaska wishes to promote in service of economic diversification.

An Alaska income tax, therefore, would have a twofold effect on small businesses: first, it would increase the direct cost of doing business in the state by imposing a new tax on small business owners’ income, and second, it would increase labor costs, since the income tax also falls on labor and this burden would be borne, to varying degrees based on employment elasticities, by both employers and employees.

Income Tax Volatility

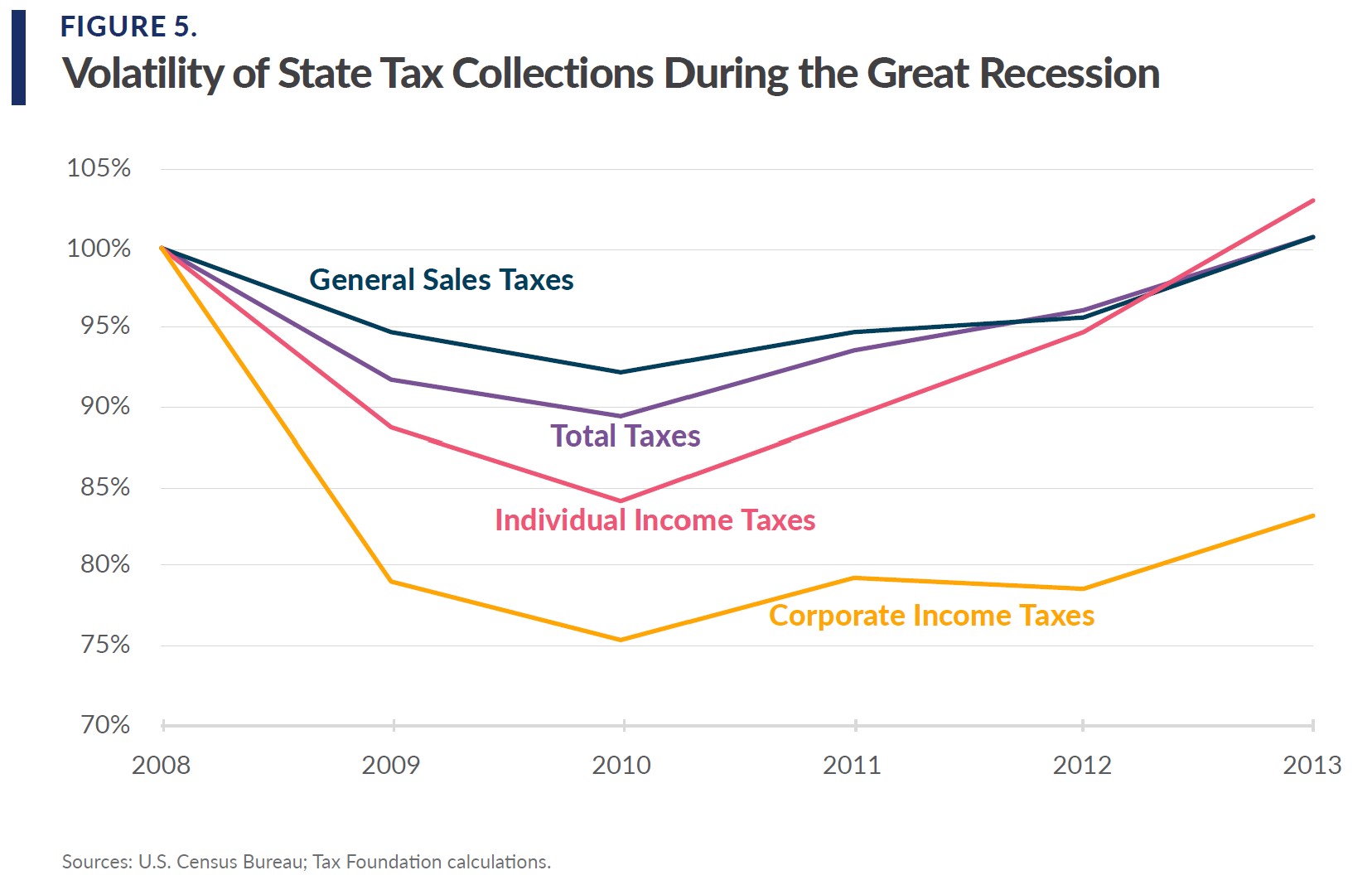

As a general rule, income taxes are more volatile than consumption taxes, as can be seen from aggregate state tax collections across the country during and immediately after the Great Recession. By 2010, general sales taxes had declined 8 percent from their 2008 peak, while individual income taxes fell 16 percent and corporate income tax collections plummeted 25 percent.19

The relative stability of sales taxes compared to income taxes is not unique to the Great Recession. While most people curtail some expenditures during an economic downturn, there is only so much they can—or are willing to—cut. Even those with no wage income continue to consume, supported by savings and governmental assistance, while those whose incomes decline are likely to reduce savings rates more drastically than consumption. Corporate income tax collections are the most volatile because, even in a deep recession, most individuals earn taxable income, whereas corporations may post actual losses and thus have no net income to tax.

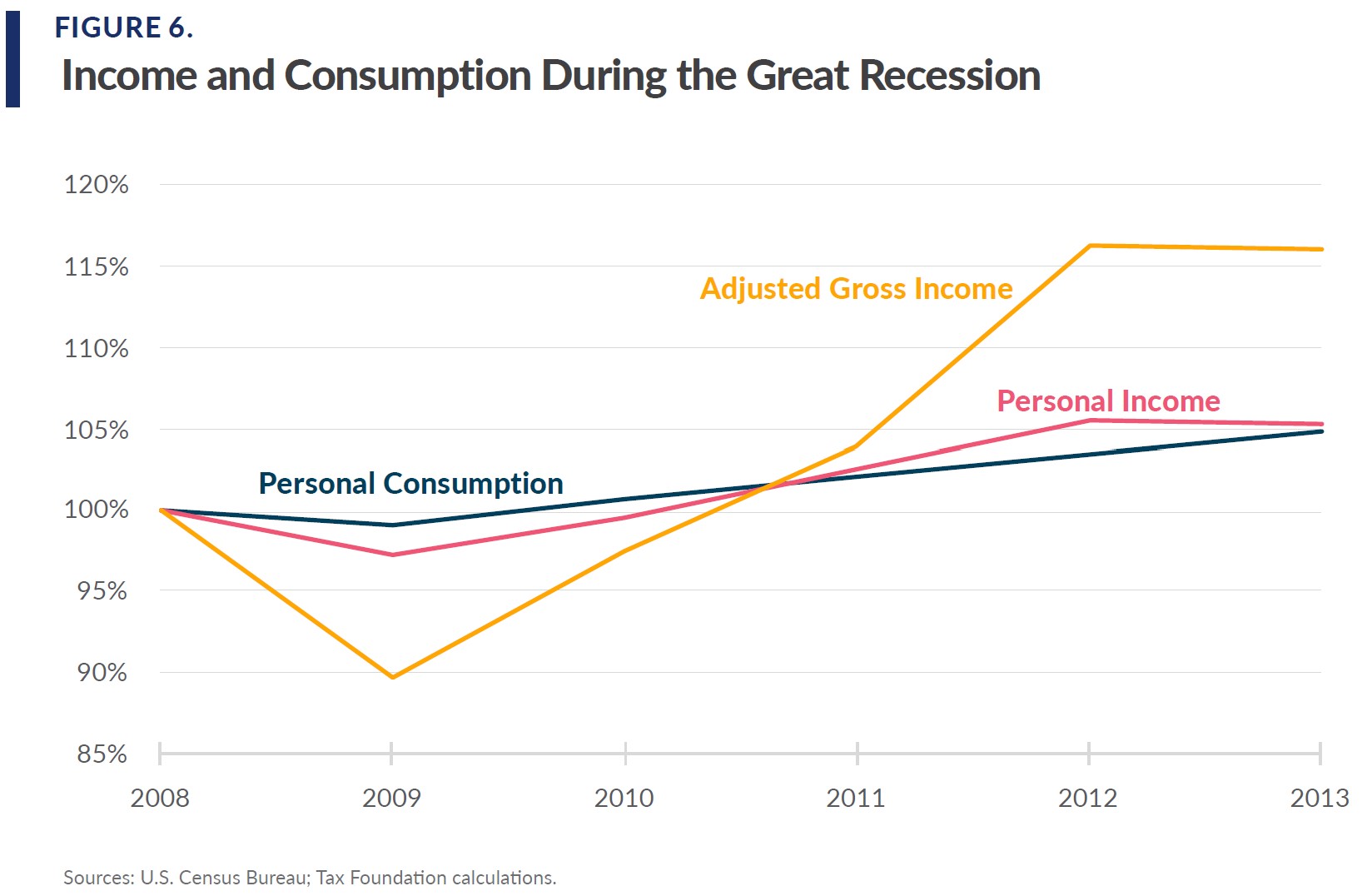

Both income and consumption fall when the economy contracts, though personal expenditures represent a greater share of income during a downturn. Figure 6 below demonstrates the changes in spending and income that underlie these fluctuations in tax collections. Personal consumption expenditures were relatively stable throughout the Great Recession while personal income declined only slightly more. Adjusted gross income proved extremely volatile. This matters for tax collections.

The U.S. measure of personal income includes income from all sources, including government. During a recession, wage, salary, and investment income declines, but (typically untaxable or at least less taxed) governmental assistance tends to rise, providing a smoothing effect. Income that is potentially taxable, however, falls sharply. Most states begin their own individual income tax calculations with adjusted gross income, and during an economic contraction, both gross income and the share of gross income that is taxable (since income below certain levels is typically excluded through deductions and exemptions) can be expected to decline.

The upshot is that income tax collections rise more rapidly than sales tax collections in good years but decline more precipitously in bad years. Income taxes are both more volatile and more cyclical than consumption taxes. States try to hedge against this reality by diversifying their other forms of tax collections, maintaining rainy day funds, and sometimes even restricting how much capital gains income in particular can be budgeted for, since capital gains realizations can vanish during an economic downturn.

Alaska’s challenge is that a potential income tax is the hedge, rather than the tax hedged against. It would be intended to help smooth over declines in taxes from the oil and gas industry and in investment returns. Unfortunately, it is a tax ill-suited for the purpose due to its own volatility.

The Economic Implications of an Income Tax

That taxes affect decision-making is among the oldest recorded observations in political economy. Some of the earliest texts in existence relate to taxes and there is evidence of tax arbitrage and tax-induced behaviors from the start. But taxes do more than simply reduce consumer wealth or purchasing power; just as important is the incentive structure created by the way taxes are imposed. Unsurprisingly, different types of taxes have distinct impacts on taxpayers and, consequently, on economic outcomes.

Every tax reduces economic returns. (Some of the government spending it facilitates, of course, may be wealth-creating.) But the effect is unequal. There is truth to the adage that “whatever you tax, you get less of,” so policymakers should think carefully about what they choose to tax, and how. Individual income taxes fall on labor and investment. On the margin, they lower the payoff to work, decreasing the supply of labor while increasing its cost, and they reduce both the returns to investment and the resources available to invest.

An income tax can be conceptualized as a tax on consumption plus the change in savings, while a well-structured sales tax is a tax on income less the change in savings. An income tax reduces the capacity for future consumption; economically, it acts like a sales tax that increases the cost of future consumption, with each additional hour of labor producing fewer goods in the future. Consumption taxes are much more economically neutral by comparison and the economic literature consistently finds that sales taxes are less of an impediment to economic growth or location decisions than income taxes.20

Consumption taxes also fall on suppliers of labor and capital, like income taxes, but they do so neutrally and—at least when well-designed—avoid double-taxing these factors. Sales taxes are typically destination-sourced, meaning that they are taxed where a good or service is consumed, not where it is produced. Thus, unlike income taxes, they do not discourage investment or job creation in a particular location.21 However, this is only true insofar as the tax falls on final consumption; when the tax falls on business inputs, it increases the cost of investing in-state.

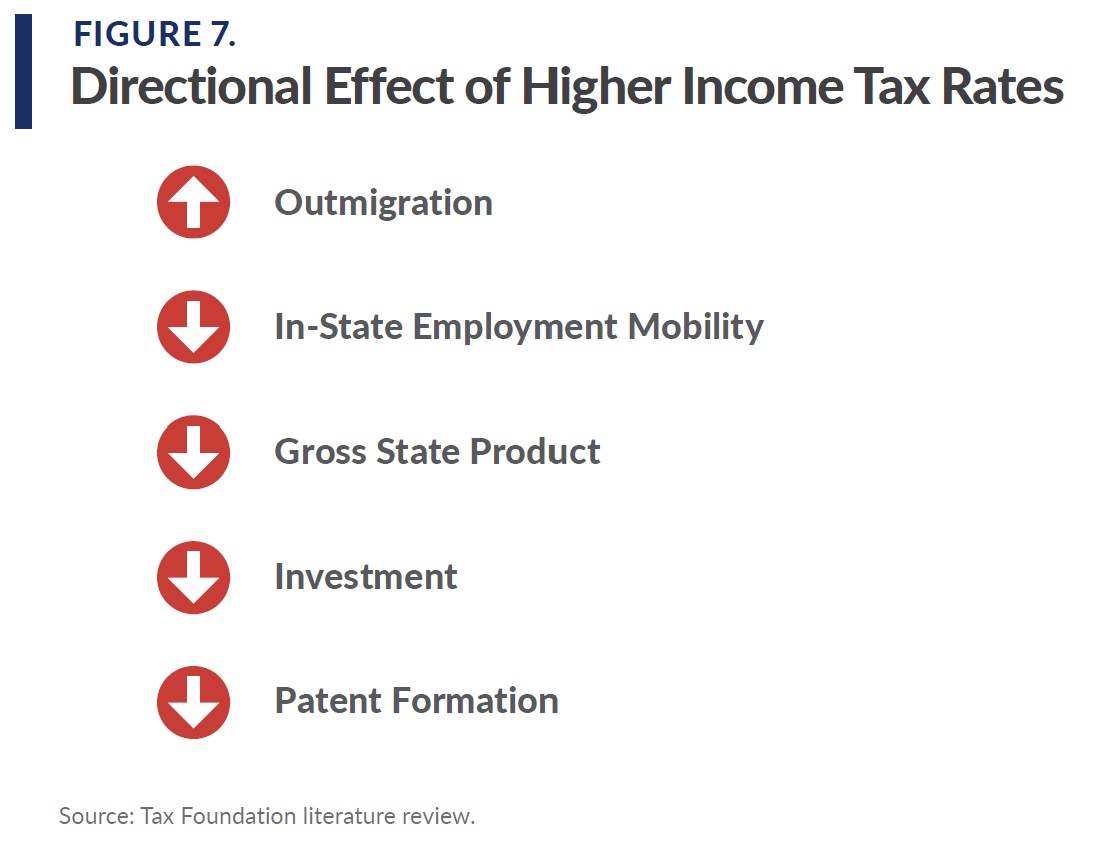

The most robust body of economic literature on income taxation focuses on relative levels, not on presence or absence, of income taxation to provide evidence of the effects of marginal changes in taxation. The literature is substantial and not monolithic in its findings, but overall, research finds that the more that income is taxed, the greater the outmigration, while the region experiences lower levels of economic growth, investment, employment mobility, and even patent formation (a good proxy for general innovation).22 Comparative evaluations likewise demonstrate that, while all taxes can have these effects to some degree, the impact is heightened with income taxes as opposed to sales or property taxes.

The most robust body of economic literature on income taxation focuses on relative levels, not on presence or absence, of income taxation to provide evidence of the effects of marginal changes in taxation. The literature is substantial and not monolithic in its findings, but overall, research finds that the more that income is taxed, the greater the outmigration, while the region experiences lower levels of economic growth, investment, employment mobility, and even patent formation (a good proxy for general innovation).22 Comparative evaluations likewise demonstrate that, while all taxes can have these effects to some degree, the impact is heightened with income taxes as opposed to sales or property taxes.

A series of papers by Organisation for Economic Co-operation and Development (OECD) economists concluded that, of all the major taxes, corporate income taxes are the most harmful to growth, followed by individual income taxes, while consumption and property taxes are less economically damaging. They found that a 1 percent shift of tax revenues from income taxes to consumption and property taxes would increase gross domestic product (GDP) per capita by as much as 1 percent in the long run, and that income taxes were more strongly associated with lower incomes than sales or consumption taxes.23

Ferede and Dahlby (2012) made the counterintuitive finding that sales tax increases are generally associated with increases in economic growth, explained by the fact that these increases often replaced income taxes and other taxes on investment, which were less pro-growth than their replacement.24

This finding was in some ways anticipated by Mark, McGuire, and Papke (2000), whose research shows that a 1 percentage point increase in a state’s individual income tax rate reduces annual population growth rates by 0.81 percentage points, while a similar 1 percentage point increase in local sales tax rates actually increases the annual growth rate by 0.83 percent, evidently because residents favor the services provided by sales taxes more than they dislike the tax—one to which they are innately less sensitive—whereas the opposite is true for income taxes.25

Nguyen, Onnis, and Rossi (2021) studied the impact of both consumption and income taxes on income, private consumption, and investment. Their research revealed that a 1 percentage point cut in the average income tax rate resulted in a 1.5 percent increase in GDP in one year’s time, along with a 4.6 percent increase in private investment and a 1.6 percent increase in private consumption.

Conversely, consumption tax cuts of the same magnitude had mostly insignificant economic effects, demonstrating the more distortionary implications of income versus consumption taxes.26 Gentry and Hubbard (2002) found that employees were less likely to move to a better job in states with high tax rates or high levels of tax progressivity, consistent with the lower return to work under high-rate income taxes. The researchers also found a sizable and statistically significant relationship between wage growth and tax progressivity, with progressive tax structures inhibiting wage growth in the state.27

Feldstein and Wrobel (1998) concluded that state and local governmental efforts to conduct redistribution through the tax code, and particularly through individual income taxes, are substantially countervailed by tax-induced migration, with a national leveling occurring as higher earners take advantage of their high levels of mobility to relocate out of states with high income taxes. Firms are also incentivized to reduce the number of higher-paying jobs while increasing the number of lower-paying jobs.28

Romer and Romer (2010) explored the relationship between tax changes and economic growth. They focused exclusively on exogenous changes—those motivated by factors other than economic stabilization—to help control for other variables that may have simultaneously influenced economic conditions. They found that “tax increases are highly contractionary,” and that an exogenous tax increase worth 1 percent of gross product (national or state) resulted in an estimated 3 percent decline in gross product after three years. They documented a large negative correlation between tax levels and both personal consumption expenditures and private domestic investment, with investment falling by 12.6 percent in response to a tax increase worth 1 percent of gross product.29

Mertens and Ravn (2013) conducted a similar study and found that a 1 percentage point cut in the average personal income tax rate yielded a 2.5 percent increase in gross product. Such a cut also yielded higher employment, peaking at 0.8 percentage points higher after five quarters, and with a higher number of hours worked per worker. Within six months of a 1 percentage point cut in the average personal income tax rate, consumption increased by 5 percent. And one year out, private nonresidential investment grew by 4 percent, with the authors concluding that cuts in the individual income tax rate are “probably the best fiscal investment” if the goal is “relatively rapid job creation.”30

Rhee (2012) examined the relationship between income tax progressivity and gross production. He found that the effects were significant, but not immediate: it takes time for individuals and businesses to respond to changes in the tax code. Therefore, changes in gross state product were not contemporaneous with the tax change, but (unsurprisingly) lagged it, as economic decisions began to be affected by the higher income taxes.

Rhee’s study did not identify a statistically significant relationship between progressivity and migration (though other studies have found one), but he suggests an offsetting effect. Essentially, states with high-rate or highly progressive income taxes may see out-migration of high-income individuals offset by the in-migration of lower-income individuals. This appears to be borne out by other studies, which find that high-rate income taxes have the greatest effect on the location decisions of high earners—particularly of entrepreneurs, who tend to be the most sensitive to higher levels of taxation.31

Cloyne (2013) studied tax changes in the United Kingdom, but with findings relevant to taxation elsewhere, finding that on average, a 1 percentage point cut in taxes as a proportion of GDP increases GDP by 2.5 percent after about three years. Such cuts are also associated with a 3.3 percent increase in wages above ordinary trends. Two years in, investment increased by 4.6 percent and consumption rose by 2.9 percent. 32

Mertens and Olea (2013 and 2017) found that high earners are the most sensitive to changes in tax rates, though low earners respond to tax rate changes as well, just with reduced intensity. The researchers found that pass-through business income is especially responsive to individual income tax rates and that cuts in marginal rates led to increases in gross product, decreases in the unemployment rate, and an increase in the aggregate hours worked. The latter change reflected a combination of greater employment levels and an increase in hours worked by those already employed as the return to labor increased.33

Notably, Mertens and Olea also provide evidence that marginal rates are what matter. They found that changes in marginal tax rates led to nearly proportional responses even if the average tax rate remained the same, while reductions in average tax rates without a decrease in top marginal rates did not have any statistically significant effect. While there are certainly meaningful real-world benefits to low rates on lower levels of income, the economic decisions with the greatest bearing on economic growth occur at higher income levels. As always, decisions happen at the margin—but they do not remain there. The authors found that even when tax policies only directly benefited higher earners, they induced an increase in average incomes of lower earners as well.34

Finally, Akcigit et al. (2018) found that state income taxes have pronounced negative effects on innovation, measured by the number of patents filed and the number of investors living in a state.35 These studies only scratch the surface of the literature on the economic effects of taxation, and of income taxes in particular, but they are broadly representative. Income taxes (and increases in income taxation) are associated with significant reductions in gross product, employment, investment, consumption, and innovation, while the effects of sales taxes are far less pronounced. Both taxes remove money from the private sector economy, which necessarily has an impact, but income taxes change incentive structures in ways that sales taxes largely avoid. The difference is profound.

Most states impose both an individual income tax and a sales tax. But of those with only one of the two, more states opt for a sales tax than an income tax—for good reason. If Alaska needs additional tax revenue, policymakers should bear in mind the distinct economic ramifications of each form of tax. Though Alaska is an extraordinary state, it faces meaningful economic challenges. An income tax would double down on the factors that impede the state’s economic growth.

The Sales Tax Alternative

Forty-five states impose state-level sales taxes, and 37 states permit local sales taxes. Nine states have state-level sales taxes but prohibit local sales taxes. Alaska is the only state with municipal but not state-level sales taxation.

Most states adopted their sales taxes well before Alaska’s statehood and all of the current 45 had done so by 1969. Since then, Alaska, Delaware, Montana, New Hampshire, and Oregon (often listed out of alphabetical order to create the acrostic NOMAD) have held out, though that resolve has begun to weaken in Montana, while some opponents of Oregon’s gross receipts tax would rather adopt a sales tax.

Should Alaska consider a major new tax, the sales tax has advantages over an income tax. Because the tax is largely collected by retailers, not individuals, tax administrators deal with far fewer payors—a genuine concern in a large, sparsely populated state where administration and enforcement can be costly. Because it is imposed on consumption rather than labor or investment (in contrast to an individual income tax), its economic impact is smaller and collections are less volatile than under an income tax. Adopting a state sales tax would also provide a chance to unify collection and administration—a challenge and an opportunity.

Both an income and sales tax provide opportunities for tax exporting, where a portion of the tax is paid by nonresidents. With an income tax, nonresidents would be taxed on income earned while present in the state, which can be significant in a state notable for its seasonal employment patterns. These revenues would be partially offset by the credit Alaska would have to offer its own residents for taxes they pay to other states when living or working elsewhere for a portion of the year.

With a sales tax, the exported tax burden will come from purchases by nonresident workers, tourists, and others visiting the state. It is important to note that under a typical destination-sourced sales tax, the tax would be imposed on any purchase made in Alaska—even if ordered from an out-of-state business—but not on transactions flowing from Alaska to other states. The upshot of this approach, which is the norm in other states, is that Alaska businesses are not disadvantaged when selling to consumers in other states, and Alaska consumers cannot engage in tax arbitrage by buying from an out-of-state company.

Most other states get destination sourcing right, but often fall short in their definition of sales tax bases. Were Alaska to adopt a state sales tax, this would represent an opportunity to design a clean tax code from scratch, rather than importing the detritus that comes with nearly a century of tinkering in many states. No tax code will ever be completely pure, but by entering the game late, Alaska policymakers would have the opportunity to learn from other states, avoiding the pitfalls they have encountered and bypassing the accretion of special interest exemptions that have filled most states’ tax codes over the decades.

Public finance scholars broadly agree on the following principles and observations of sales taxation, which we have articulated previously as Alaska has contemplated its tax options:

- An ideal sales tax is imposed on all final consumption, both goods and services.

- An ideal sales tax exempts all intermediate transactions (business inputs) to avoid tax pyramiding.

- Sales taxes should be destination-based, meaning that tax is owed in the state and jurisdiction where the good or service is consumed.

- The sales tax is more economically efficient than many competing forms of taxation, including the income tax, because it only falls on present consumption, not saving or investment.

- Because lower-income individuals have lower savings rates and consume a greater share of their income, the sales tax can be regressive, though broader bases that include consumer services (much more heavily consumed by higher-income individuals) push in a progressive direction.

- The sales tax scales well with the ability to pay principle because it grows with consumption and is therefore more discretionary than many other forms of taxation.

- Consumption is a more stable tax base than income, though the failure to tax most consumer services in many states is leading to a gradual erosion of sales tax revenues as services become an ever-larger share of consumption.

Most states impose their sales taxes on bases that consist of most goods—with economically significant policy carveouts—and relatively few services. With limited exceptions, most state sales taxes are imposed on transactions involving tangible property: appliances but not apps, light fixtures but not landscaping. This was less a conscious choice than an accident of history, a relic of the fact that so many sales taxes were imposed during the Great Depression, when services comprised a far smaller share of the economy. It was administratively simpler in that earlier era to focus almost exclusively on retail sales, and even the later ones tended to follow their lead.

Elsewhere, states grapple with questions that Alaska could answer from the start. In other states, e-books might be untaxed while paperbacks are taxable. A trip to a hair salon might yield a taxable purchase of a bottle of conditioner, while the services of the hair stylist are tax-exempt. Personal services, in particular, tend to go untaxed, largely as a historical accident. And that is significant, especially as we transition to an ever more service-oriented economy.

Sales taxes should be broad-based in service of both economic neutrality and tax equity. That is, they should not pick winners and losers firstly because the tax code should not unnecessarily interfere with economic decision-making by favoring some transactions and some sellers over others. It should also avoid picking winners and losers because this is a potential source of tax regressivity.

Sales taxes have two potential sources of regressivity: one, the propensity of lower-income individuals to consume a greater share of their income, and two, a scope of taxable consumption that is more likely to fall on the sorts of transactions that dominate the consumption of lower- and middle income individuals.

Policymakers often exempt or lower rates on certain classes of consumption as a progressive reform. The exemptions many states provide for groceries are one such example—though there is reason to believe it may be ineffective. Prepared foods are taxed at the standard rate and most of the regressivity of taxing unprepared foods is addressed by the exemption for Supplemental Nutrition Assistance Program (SNAP) and Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) purchases, while the exemption is enjoyed by high-income earners as well—who often spend considerably more on groceries.

In fact, analysis by the Tax Foundation and others shows that lower-income taxpayers are actually better off if groceries are included in sales tax bases (with exemptions for SNAP and WIC purchases consistent with federal requirements), allowing for a lower sales tax rate, than if the overall rate is higher but groceries are exempt.36 The lower grocery rate is designed to create progressivity but largely fails to do so.

There is a more straightforward way to promote equity within the sales tax: taxing personal services. Consumption of personal services tends to be more discretionary than consumption of goods. Consequently, higher-income individuals spend a greater share of income on services, which are frequently untaxed. Unfortunately, most existing state sales taxes are levied on all tangible property (goods) unless expressly exempted, but only apply to services if expressly enumerated in the statute.

States have been gradually expanding their sales tax bases, but tax policies are frequently path dependent. Expanding the sales tax base to new transactions can be nearly as difficult as creating the tax in the first place. Should Alaska opt to impose a sales tax, the state should begin with as broad a base of personal consumption as possible, avoiding politically challenging battles down the road. In so doing, policymakers would adopt a more stable sales tax than that which exists in most other states while avoiding the accidental wrongs that favor some transactions over others and tend to favor the wealthiest consumers.

At the same time, Alaska policymakers implementing a sales tax would want to avoid the taxation of intermediate (rather than final) transactions. To varying degrees, business-to-business transactions are taxed in every state with a sales tax, meaning that the sales tax is often embedded in the final price of a good or service several times over. This is not an ineluctable law of consumption taxes, but it has unfortunately been the reality in the United States (one of the country’s departures from how consumption taxes are implemented in Europe and elsewhere).

A well-structured sales tax is imposed on all final consumer goods and services while exempting all purchases made by businesses that will be used as inputs in the production process. This is not because businesses deserve special treatment under the tax code, but because applying the sales tax to business inputs results in multiple layers of taxation embedded in the price of goods once they reach final consumers, a process known as “tax pyramiding.” The result is higher and inequitable effective tax rates for different industries and products, which is both nonneutral and nontransparent, hiding actual tax costs from consumers.

Not only would Alaska have an opportunity to create a broad base from the start, making it more immune to erosion than other states’ tax codes, but doing so would also yield the opportunity to standardize municipal sales taxes.

From the standpoint of compliance, administration, and good government, this is desirable—though admittedly quite difficult. Alaska municipalities have gone their own way for many years, and a state-established sales tax base, with state-run collections and disbursement, would shake up the status quo. Still, a state-administered sales tax (the norm in other states) would dramatically reduce compliance costs while increasing compliance rates.

Seasonal Taxation

For everything there is a season—including taxes. But whereas “tax season” is traditionally just when most people pay their taxes, some Alaska policymakers have toyed with the idea of making tax liability seasonal as well, tracking the influx of tourism or seasonal workers. This model already exists at the municipal level, with cities like Nome and Ketchikan increasing sales tax rates during the summer tourism season and lowering them for the rest of the year. Theoretically, the same approach could be deployed at the state level, or the tax could be toggled on and off entirely based on the season.

But what is theoretically possible is not necessarily good tax policy. Alaska is not the first state to explore a two-tier tax system that increases exporting to non-residents, but toggling a tax on and off would be new. States usually take more modest steps, like creating a homestead exemption for owner-occupied property but not for other property (which would include vacation homes) or having income tax deductions and exemptions that are only available to state residents, but these approaches do not vary with the calendar.

Constitutionally, states may not discriminate against nonresidents in taxation. For instance, states could not create an income or sales tax that only applied to nonresidents. They may, however, put a thumb on the scale in favor of residents in lesser ways, or choose tax regimes that functionally favor residents. The courts must adjudicate whether a particular tax’s design goes too far in targeting nonresidents, but the seasonal sales tax model, while unusual, has prevailed in some Alaska jurisdictions and is at least not presumptively unconstitutional.

It is, however, complex and likely to influence consumer behavior in significant ways. If the sales tax only exists for six months out of the year, then residents will be strongly incentivized to delay making large purchases until the sales tax is in abeyance. Unless different rules exist for different products, which creates even more complexity, one would expect Alaskans to deny themselves big-ticket items like automobiles, appliances, and large electronics during the months when the sales tax is in effect, waiting for the rate to zero out.

A seasonal sales tax would, therefore, reduce revenues more than would be expected simply by subtracting out certain months of sales. It could also create inventory bottlenecks, as consumer demand for more costly consumer goods fluctuates by season, and introduce added regressivity into the sales tax, since items that could be most easily shifted into the tax-free season would tend to be more discretionary (and sometimes luxury) purchases, whereas everyday purchases would not lend themselves as easily to such tax arbitrage.

Furthermore, if Alaska wants to collect revenue from remote sellers—as surely it would—this complexity would create substantial compliance burdens and preclude the state from joining the plurality of sales tax-collecting states in the Streamlined Sales Tax Governing Board, which exists to simplify multistate sales and use tax collections and remittance and guarantee a certain level of uniformity in how sales taxes work.

While seasonal sales taxes do exist at the municipal level in Alaska, they are far from the norm, meaning that local sales taxes might be owed year-round on transactions while state sales taxes are only in place during certain months. This approach would throw a wrench in any plans to consolidate sales tax administration at the state level. Right now, Alaska’s municipal sales taxes must be complied with separately for in-state sellers, though a system has been introduced to simplify the process for remote sellers. Even then, sales tax bases vary by jurisdiction.

Only three other states—Alabama, Colorado, and Louisiana—have varying sales tax bases or local autonomy in sales tax administration, and all three recognize it as a substantial impediment to tax compliance and are making efforts to consolidate administration at the state level, consistent with the practice of all other states with local option sales taxes. Alaska should seek to do the same—but a seasonal sales tax would stand in the way.

Conclusion

Alaska policymakers are understandably concerned about the long-term viability of the state’s overwhelming reliance on the oil and gas industry for revenue, but the state’s unique economy and geography, and low population density make some of the “traditional” taxes less efficient than they might be elsewhere. Any major tax will be more burdensome in Alaska than in a state with a more typical economy but, of the options, an individual income tax is the greater threat to Alaska’s future prosperity.

Alaskans already pay more in federal income taxes than their peers in the lower 48 states on identical purchasing power, and a state income tax could undercut the diversification and growth of the state’s economy. The economic literature is clear that income taxes are more economically damaging than sales taxes. And the economic harms appear more significant considering the relatively modest increase in state revenue that could result from the imposition of such a tax.

Alaska policymakers will face difficult choices in the coming years. Yet their aversion to adopting an income tax rests on sound principles. They are right to treat it as the least attractive option.

Endnotes

- U.S. Bureau of Labor Statistics, Civilian Labor Force Participation Rate dataset, https://www.bls.gov/.

- Alaska Department of Revenue, Tax Division, Revenue Sources Books and Forecasts, multiple years, http://tax.alaska.gov/programs/sourcebook/index.aspx.

- For revenue data and projections, see Alaska Department of Revenue, “Spring 2022 Revenue Forecast,” March 15, 2022, http://tax.alaska.gov/programs/documentviewer/viewer.aspx?1722r.

- There are data availability limits for some of the early years of statehood, which would insert a certain amount of guesswork into averages. Beginning with 1966 rather than 1959 avoids these data gaps.

- Alaska Stat. § 37.05.540.

- Alaska Const. art. IX, § 16.

- Tax Foundation calculations based on U.S. Bureau of Economic Analysis data.

- Katherine Loughead and Jared Walczak, “States Respond to Strong Fiscal Health with Income Tax Reforms,” Tax Foundation, July 15, 2021, https://taxfoundation.org/2021-state-income-tax-cuts/; Timothy Vermeer, “State Tax Reform and Relief Enacted in 2022,” Tax Foundation, July 13, 2022, https://taxfoundation.org/state-tax-reform-relief-enacted-2022/.

- The average fell by a similar amount, 1.9 percent.

- New York separately accelerated a rate reduction for middle- and upper-middle-income earners and adopted a new higher rate on high earners. The state is included here as raising rather than cutting rates, though arguably it did both.

- Jared Walczak, “States Inaugurate a Flat Tax Revolution,” Tax Foundation, Sept. 7, 2022, https://taxfoundation.org/flat-tax-state-income-tax-reform/.

- Ronald Sullivan, “Final Attempt to Enact Jersey Income Tax Fails,” The New York Times, May 16, 1975, https://www.nytimes.com/1975/05/16/archives/finalattempt-to-enact-jersey-income-tax-fails-last-ditch-attempt.html.

- Janelle Fritts, “Facts & Figures 2022: How Does Your State Compare?” Tax Foundation, March 29, 2022, https://taxfoundation.org/publications/facts-and-figures/.

- Ken Girardin, “Revenue Ratchet: Connecticut’s Income Tax at 30,” Yankee Institute, March 29, 2021, https://yankeeinstitute.org/2021/03/29/revenue-ratchet-connecticuts-income-tax-at-30/.

- Jorge Barro, Joseph Bishop-Henchman, and Russ Latino, “Better Jobs Mississippi: Tax Structure for Growth,” Empower Mississippi, https://empowerms.org/wp-content/uploads/2021/02/Better-Jobs-report-.pdf.

- Alaska Department of Revenue, Tax Division, “Annual Report 2021,” http://tax.alaska.gov/programs/programs/reports/AnnualReport.aspx?Year=2021. The figure rose to 19,672 in FY 2021, but comparable FY 2021 data are not available at the federal level.

- Internal Revenue Service Statistics of Income, Historic Table 2, https://www.irs.gov/statistics/soi-tax-stats-historic-table-2.

- U.S. Small Business Administration Office of Advocacy, “2020 Small Business Profile: Alaska,” https://cdn.advocacy.sba.gov/wp-content/uploads/2020/06/04142939/2020-Small-Business-Economic-Profile-AK.pdf.

- Jared Walczak, “Income Taxes Are More Volatile Than Sales Taxes During an Economic Contraction,” Tax Foundation, March 17, 2020, https://taxfoundation.org/income-taxes-are-more-volatile-than-sales-taxes-during-recession/.

- See Joseph Bankman and David A. Weisbach, “The Superiority of an Ideal Consumption Tax over an Ideal Income Tax,” Stanford Law Review 58:5 (April 2010): 1413; and Jens Matthias Arnold, Bert Brys, Christopher Heady, Åsa Johansson, Cyrille Schwellnus, and Laura Vartia, “Tax Policy for Economic Recovery and Growth,” The Economic Journal 121:550 (February 2011): F59-F80.

- Douglas L. Lindholm and Karl A. Frieden, “After Wayfair: Modernizing State Sales Tax Systems,” State Tax Notes, May 14, 2018, https://cost.org/globalassets/cost/state-tax-resources-pdf-pages/cost-studies-articles-reports/after-wayfair-modernizing-state-sales-tax-systems.pdf.

- The brief survey of the literature that follows is partially adapted and abridged from Timothy Vermeer, “The Impact of Individual Income Tax Changes on Economic Growth,” Tax Foundation, June 14, 2022, https://taxfoundation.org/income-taxes-affect-economy/.

- Åsa Johansson, Christopher Heady, Jens Arnold, Bert Brys, and Laura Vartia, “Tax and Economic Growth,” OECD Economics Department Working Papers No. 620 (2008); Jens Arnold, “Do Tax Structures Affect Aggregate Economic Growth? Empirical Evidence from a Panel of OECD Countries,” OECD Economics Department Working Papers No. 643 (2008).

- Ergete Ferede and Bev Dahlby, “The Impact of Tax Cuts on Economic Growth: Evidence from the Canadian Provinces,” National Tax Journal 65:3 (September 2012): 563-594.

- Stephen T. Mark, Therese J. McGuire, and Leslie E. Papke, “The Influence of Taxes on Employment and Population Growth: Evidence from the Washington, D.C. Metropolitan Area,” National Tax Journal 53:1 (March 2000): 114-116.

- Anh D.M. Nguyen, Luisanna Onnis, and Raffaele Rossi, “The Macroeconomic Effects of Income and Consumption Tax Changes,” American Economic Journal: Economic Policy 13:2 (2021): 439-66.

- William M. Gentry and R. Glenn Hubbard, “The Effects Of Progressive Income Taxation On Job Turnover,” Journal of Public Economics 88:9 (2002): 2301-2322.

- Martin Feldstein and Marian V. Wrobel, “Can State Taxes Redistribute Income?” Journal of Public Economics 68:3 (1998): 369–96.

- Christina D. Romer and David H. Romer, “The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks,” American Economic Review 100:3 (2010): 763-801.

- Karel Mertens and Morten O. Raven, “The Dynamic Effects of Personal and Corporate Income Tax Changes in the United States,” American Economic Review 103:4 (2013): 1212-47.

- Tae-hwan Rhee, “Macroeconomic Effects of Progressive Taxation,” (November 2012), https://www.aeaweb.org/conference/2013/retrieve.php?pdfid=394.

- James Cloyne, “Discretionary Tax Changes and the Macroeconomy: New Narrative Evidence from the United Kingdom” American Economic Review 103:4 (2013): 1507-28.

- Karel Mertens and Jose L. Montiel Olea, “Marginal Tax Rates and Income: New Time Series Evidence,” Quarterly Journal of Economics 133:4 (2018): 1803–1884.

- Ibid.

- Ufuk Akcigit, John R. Grigsby, Tom Nicholas, and Stefanie Stantcheva, “Taxation and Innovation in the 20th Century,” NBER Working Paper No. 2498 (2018), https://scholar.harvard.edu/stantcheva/publications/taxation-and-innovation-20th-century.

- Jared Walczak, “The Surprising Regressivity of Grocery Tax Exemptions,” Tax Foundation, April 13, 2022, https://taxfoundation.org/sales-tax-grocery-tax-exemptions/.