By Aubrey Wursten

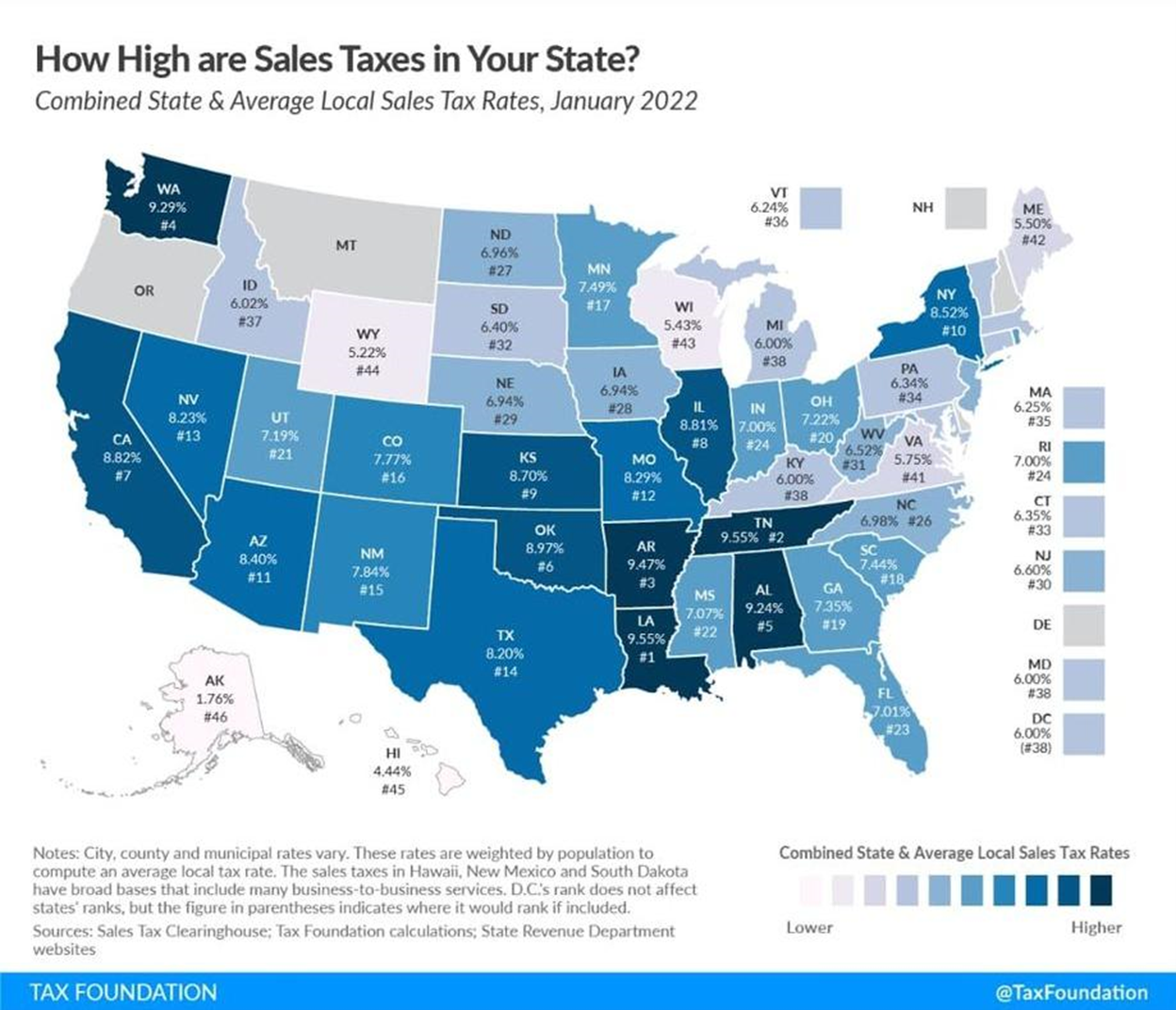

Sales tax levels and structure affect the spending habits of both companies and consumers, and states with low and simple sales tax schemes have a distinct advantage over their counterparts. In states where this tax burden is low and equally applied, owners are more likely to bring their businesses, and buyers are more likely to spend their money. And according to a recent analysis by the Tax Foundation, Alaska earns high marks for its reasonable sales tax system. It ranks an impressive 5th place out of the 50 states, with a score of 8.8 out of 10.

Lower sales taxes encourage businesses in multiple ways. Notably, prospective owners are more likely to open a business where they can keep a high percentage of the ticket price, instead of handing it to the government. Consumers are only willing and able to pay a certain amount for any product, and if a large portion of that cost is sales tax, the business will see little profit. Because Alaska has no state sales tax (although the existence of some local sales taxes effectively renders the statewide rate to 1.7%), it offers an entrepreneur an obvious advantage.

Even-handed application of a state’s tax code also provides an incentive for businesses to operate in the area. If one particular item has a high excise tax proprietors know that they will either have to narrow their profit margins on that one item or risk selling less of it. Consequently, if that high-tax product suddenly overtakes other products in popularity, their overall profit margins will plummet. This is both a risk and a complication that will lead businesses to operate elsewhere.

Although Alaska does have excise taxes on multiple products, the same is true of even the states that beat them on the Tax Foundation’s scorecard. However, the passage of bills such as the recent SB 45, which will impose an excise tax of 75% on vape products, indicates that Alaska may not be as averse to “sin taxes” as their 5th-place standing might indicate. Business owners will likely take this into consideration when deciding whether to operate in the state.

It is worth noting that both the level and simplicity of sales taxes also have an effect on remote businesses. Although the Supreme Court has ruled that all large businesses are subject to local sales tax, many states have so-called “safe harbor” laws that allow small out-of-state companies to enjoy many of the benefits of having a brick-and-mortar store in the state. In the era of widespread online shopping, this is more attractive to sellers than it ever has been. However, Alaska fared worse than some states in this area, due to their failure to enforce “uniform administration.” Because Alaska has some local sales taxes, out-of-state businesses may find themselves in a sort of tax limbo. This leads to uncertainty for out-of-state businesses.

Of course, most people are not business owners, but customers. However, any benefits to a business tend to translate to advantages for the consumer. More businesses mean more competition, both in prices and variety of inventory. If multiple similar shops open in an area, each will be forced to keep prices low and options plentiful in order to retain customers.

Avoiding random excise taxes also benefits consumers. Although this type of charge is often used as a “vice tax,” aimed at discouraging negative behaviors, one can easily argue that such taxes often fail at their stated motive. As the Tax Foundation points out, “For example, if an excise tax on soda is justified by its high sugar content, then the tax should be on sugar in general to account for 1) other products with high sugar content and 2) the variable amount of sugar—and affiliated cost to society—in different sodas.”

Excise taxes rarely take so many different issues into account, which ultimately renders them unhelpful. (And if they did indeed take these other aspects into consideration, the costs and inconvenience of enforcing such laws would likely make them counterproductive.) Furthermore, statistics show that excise tax burdens disproportionately affect customers earning lower wages, which effectively prices consumers out of the market.

For multiple consecutive years, Alaska has maintained its 5th place position on the sales tax chart. It would do well to stay the course if it wants to remain competitive in the national market. Although it faces historical budget challenges, especially in the wake of COVID-19 fallout, Alaska should avoid giving in to the misguided temptation to jump first to taxes to fill the gap when revenue falls. Any funding problems should first be combated with responsible spending, not by reversing the admirable tax restraint that has been successful for both Alaskan businesses and consumers.

To bolster its state rating even further, the municipalities in Alaska with a local sales tax might reconsider that choice if the opportunity arises. In addition, Alaska should be mindful of possible negative impacts of excise taxes. And finally, the legislature should clarify its out-of-state sales tax laws, to increase confidence of owners potentially affected by them. A fifth-place ranking is an impressive feat, and Alaska has what it takes to be even higher.

*******

Aubrey Wursten is Alaska Policy Forum’s Summer 2022 policy intern. She is currently studying Applied Health at Brigham Young University-Idaho.