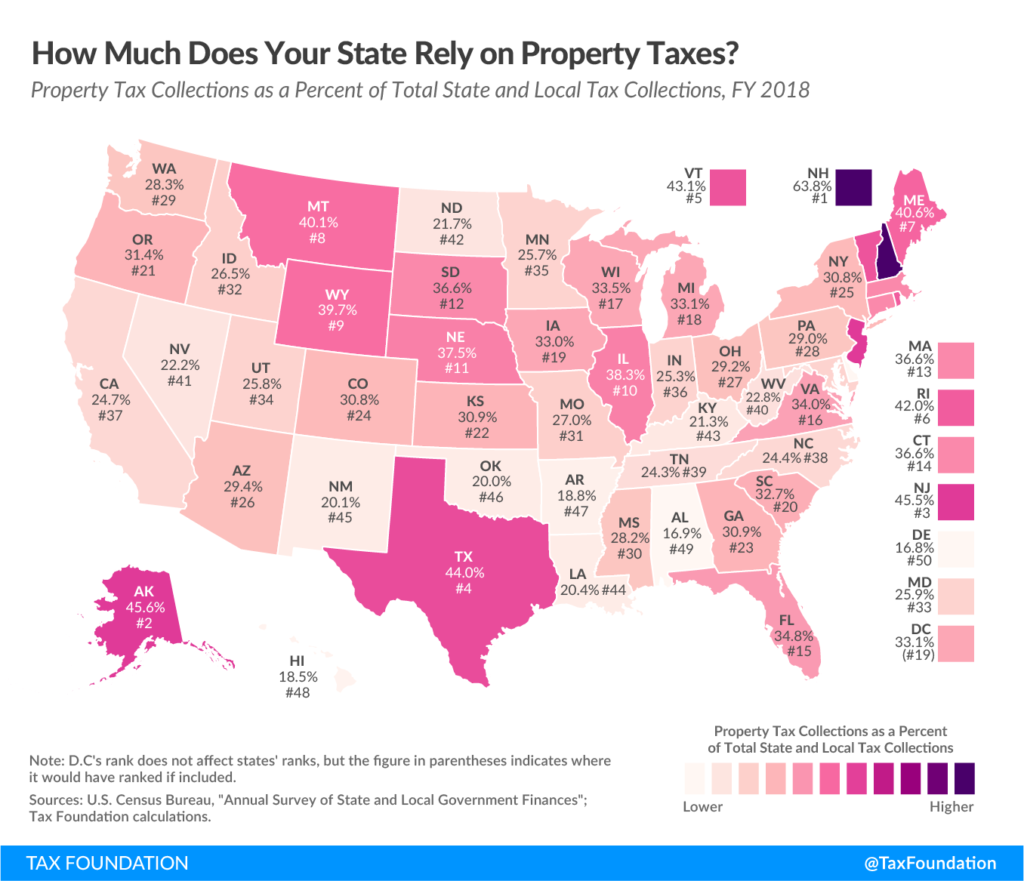

The Tax Foundation has released a series of articles examining the reliance of state budgets on property taxes, sales taxes, and individual income taxes. Alaska does not yet have an income tax on individuals, although several bills have been introduced in the 2021-2022 legislative session to impose an income tax. Similarly, Alaska does not have a statewide sales tax, though localities can and sometimes do impose one. This post will focus on The Tax Foundation’s comparison of property taxes in the fiscal year 2018 in each state; Alaska ranked second and property taxes comprised nearly 46 percent of total state and local tax collections.

Property taxes are a significant source of revenue for states and the largest source of tax revenue for localities. Nationwide in FY18, property taxes consisted of 72 percent of local tax collections and 31 percent of total U.S. state and local tax collections, which is a greater proportion than any other source of tax revenue. Property taxes were the largest share of local revenue in all but two states, Arkansas and Louisiana, which rely heavily on high local sales taxes. Property taxes are usually based on the fair market value of a property, while in commercial cases property taxes are based on income potential, with Alaska imposing rate limits and levy limits which serve to constrain property tax growth. Property taxes are determined by a variety of local political subdivisions, including boroughs, cities, school boards, fire departments, utility commissions, and more.

Alaska ranked second for the percent of total state and local tax collections that are property taxes, with property taxes accounting for nearly 46 percent of tax collections in FY18. Notably, in Alaska not all local jurisdictions impose property taxes; taxes on the property of oil and gas producers provide an ample substitute in those jurisdictions. Alaska was only surpassed by New Hampshire, where property taxes comprised nearly 64 percent of state and local revenue. Neither Alaska nor New Hampshire currently levies an income tax. The two states with the least reliance on property taxes are Delaware and Alabama, which each collect about 17 percent of state and local revenues through property taxes.

Though property owners in Alaska may shirk at the thought of higher-than-average property taxes, this form of taxation tends to be preferable to income and sales taxes from an economic standpoint. Heavy reliance on property taxes often is a substitute for lowered or no taxes on sales, individual income, corporate income, and excise taxes, such as in Texas and New Hampshire. Property taxes tend to be less harmful to economic growth, since income taxes disincentivize labor and savings, and sales taxes rely on current consumption. In addition, while income taxes become proportionally higher as income rises, property taxes tend to be a fixed percentage of the property’s value, and Alaska already uses two methods to constrain the growth of property taxes.

Property taxes are also more transparent than most taxes; while income taxes are typically withheld from paychecks and sales taxes are paid piecewise in hundreds of transactions each year, property owners generally have a good sense of what their property taxes are each year. In addition, property value is often related to the market value of benefits that government affords in the area, such as roads, schools, and emergency services. This, of course, is another benefit of property tax: it is largely used for local improvements, which is perhaps one of the few ways that taxpayers see tangible benefits in return for their tax dollars.

Alaska levies higher property tax instead of little or no income taxes and sales taxes and this primes the state to have an economic advantage over states that impose high taxes in all three major taxes. However, if Alaska were to implement an income tax or sales tax, it would surely discourage economic growth or tax consumption, which would only contract economic recovery after the pandemic. As unsavory as writing a large check for property taxes each year is, it is preferable to having labor and consumption disincentivized – and it helps keep your tax dollars in your local community.