Introduction

These budget blocks are a simple, straightforward way to visualize how Alaska is spending its money and from which funds that money is coming. The size of each block corresponds to the amount allocated to each state agency. The larger the dollar amount, the larger the block. All of the numbers are taken straight from the FY 2022 Enacted Operating Budget agency summaries provided to the public by the Alaska Division of of Legislative Finance.

Explanation of Terminology

The operating budget is what covers ongoing operations and expenses for the State of Alaska, or the day-to-day running of the government and state programs. According to the Office of Management and Budget (OMB), it is “annual appropriations covering ongoing operations. Appropriations are typically made for a fiscal year, with funds lapsing at the end of the fiscal year.”

Agency or Department:

- Administration (Admin)

- Commerce, Community, and Economic Development (Commerce)

- Corrections

- Education and Early Development

- Environmental Conservation (Env Cons)

- Fish and Game

- Office of the Governor (Gov)

- Health and Social Services

- Labor and Workforce Development (Labor Dept)

- Law

- Military and Veterans’ Affairs (DMVA)

- Natural Resources

- Public Safety

- Department of Revenue

- Transportation and Public Facilities

- University of Alaska

- Judiciary

- Legislature (Leg)

- Debt Service – The state pays back loans or bonds that have been issued for new projects.

- State Retirement Payments – Deposits to the pension fund for state and school district employee retirement obligations.

- Special Appropriations (Special Appro) – Bonds for tax credit purchases, Alaska comprehensive insurance program, and shared taxes, such as the salmon enhancement tax and the fisheries business tax.

- Fund Capitalization (Fund Cap) – Money set aside for various funds, such as the Community Assistance Fund and the Alaska Clean Water Fund.

- Permanent Fund – Permanent Fund Earnings Reserve Account (ERA) appropriations.

- Unrestricted General Fund (UGF) – Money with no statutory restrictions; the legislature has discretion to spend this money however it chooses.

- Designated General Fund (DGF) – Non-federal money that is statutorily designated for a specific purpose. According to the Alaska Division of Legislative Finance, “The legislature traditionally complies with designations, but may use these funds for any purpose at any time.”

- “Other” State Funds – Non-federal money that the legislature has limited discretion over.

- Federal Receipts – Funds received from the federal government.

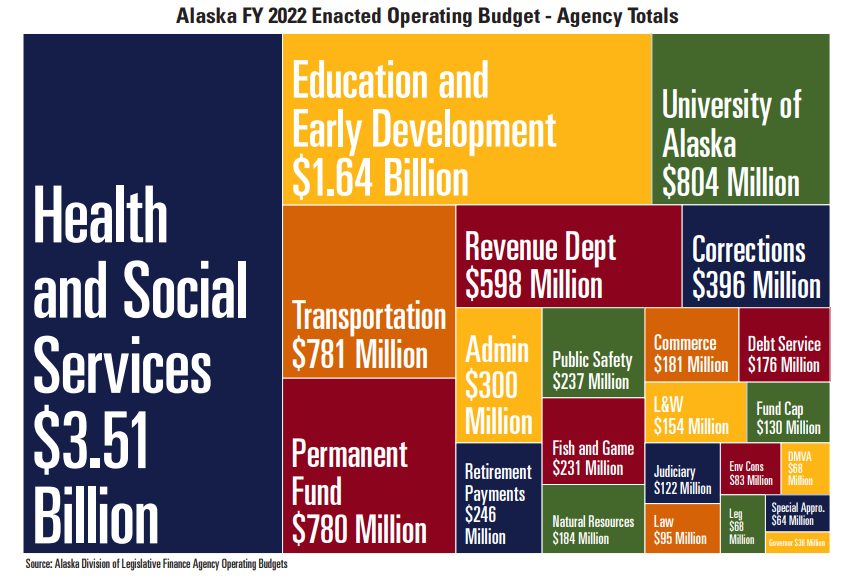

The graphic titled “Agency Totals” depicts budgeted expenses to be paid from the UGF, from the DGF, from “Other” state funds, and from federal receipts.

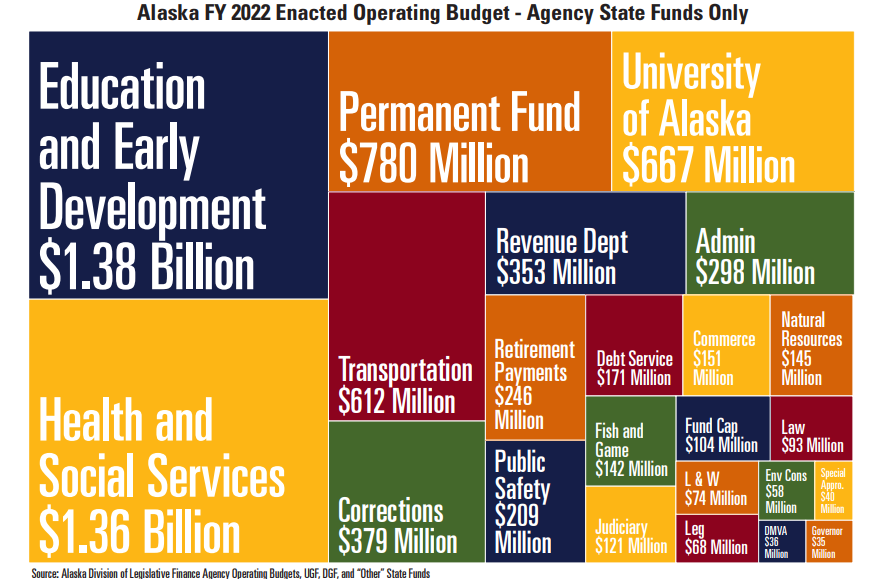

The graphic titled “Agency State Funds Only” excludes federal receipts from the agency totals.

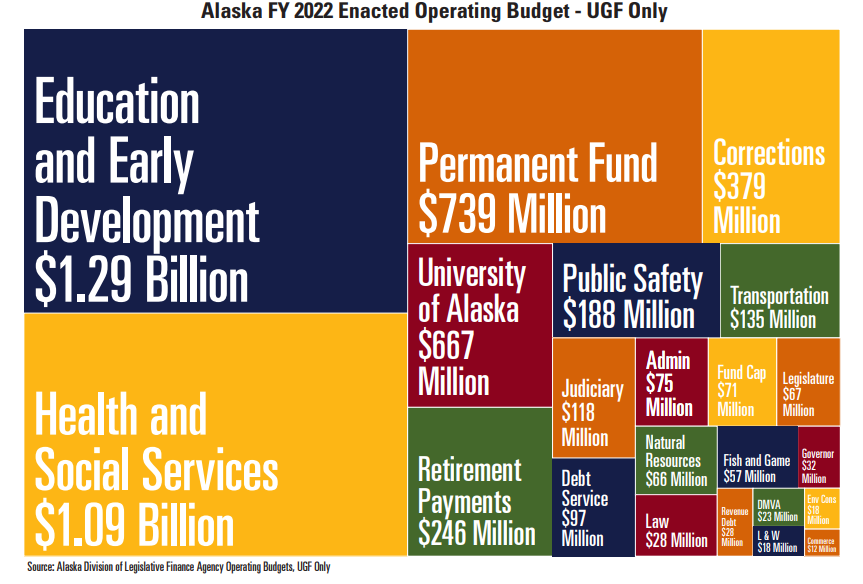

The graphic titled “UGF Only” includes only Unrestricted General Funds.

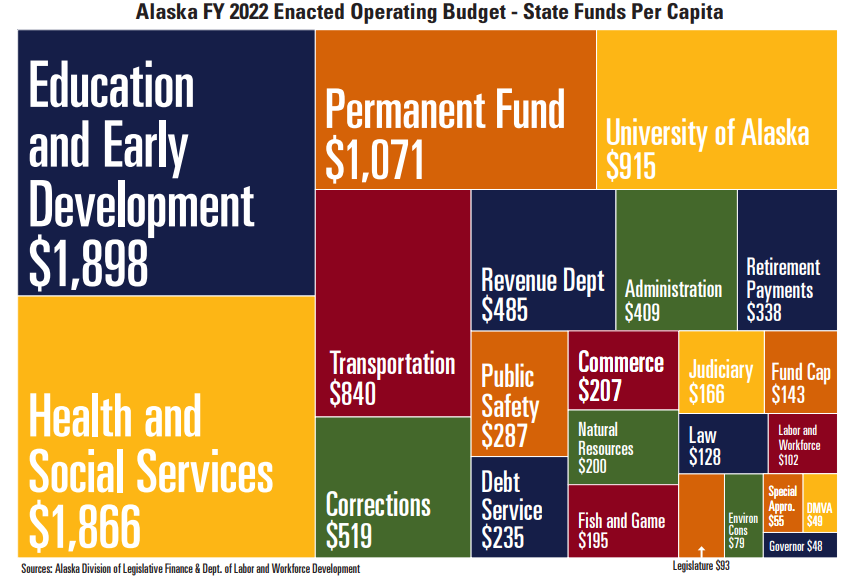

The graphic titled “State Funds Per Capita” depicts all agency budgeted expenditures from state funds (UGF, DGF, and “Other” state funds) per capita, based on Alaska’s population in 2020.